What Goes into Your Property Taxes in Lower Fairfield County?

How are property taxes calculated in Lower Fairfield County? We take you inside your property tax bill.

As communities across lower Fairfield County pass their budgets for the upcoming year, we wanted to take a look at all of the parts and pieces that go into figuring out how much you’ll pay in taxes each year. Spoiler: It’s not as simple as a city votes to increase its budget by 5% and that automatically means your taxes will go up 5%.

Let’s start by defining some of the key parts that make up how property taxes are calculated and what that means for you.

The Grand List

The best place to start when thinking about how much revenue a city can bring in is to start with its grand list, or the value of all taxable property in the city.

The grand list includes everything from massive developments, like the SoNo Collection in Norwalk to rich residential properties, like the Copper Beach Farm property in Greenwich to your house or townhouse tucked away in a neighborhood.

In general, a larger grand list typically allows a town to either collect more revenue or keep the tax rate lower. For example—using easy numbers for math purposes here!—say a city has 100 properties in year one. The burden for funding the city is split among those 100 owners. But say in the next year, 10 new properties are added. Now the city budget is split among 110 properties, ideally lessening the individual tax burden for each property owner.

Governor Ned Lamont often references this principle, stating he wants Connecticut to have “more new taxpayers, not more new taxes.”

Greenwich has the highest grand list in the state—and also one of the lowest mill rates in the region (we’ll get to that in a minute!), which allows it to have a large city budget without having a high tax rate on each individual property.

Revaluation

The next part is determining the actual value of each of those properties. According to Connecticut state statute, every five years a community is required to update the values of the properties on its grand list, known as a “revaluation.” The goal of this is to capture the most accurate value of properties at that given time. But it also means there can be dramatic swings in property values, depending on some external factors.

For example, Norwalk conducted a revaluation of its properties in 2022. At that time (and still a little to this day), the residential housing market was hot. People looking to move into the city were bidding way above the listing price on homes, driving up the value of residential housing. At the same time, coming out of the COVID-19 pandemic, commercial property values took a hit. Office spaces sat empty, people weren’t going out to restaurants or to shop in person the same way they used to leading to businesses closing.

All of that combined shifted the property tax burden in the city. Prior to the revaluation, residential housing covered about 60-65% of the tax burden; following the revaluation it was 70%. That meant, even if the city had not increased its budget that year, residents would have seen a tax increase because they were responsible for more of the taxes.

Appraised Property Value

But what exactly does this look like in practice? There are two main property values related to each parcel in the city—what the property is appraised at and what the property is taxed at.

If you’re looking to buy a home, usually you’ll hire an appraiser who, based on a number of factors including the condition of the property itself, the value of similar properties, and others, determines the value of it. The city does this too during its revaluation process. Properties that have been upgraded or are in very desirable neighborhoods often see their appraised values rise, while homes that are falling into disrepair, will see their values drop.

Once you have the appraised value of a property, then there’s the assessed value, which is what you pay taxes on. The assessed value is 70% of the appraised value. This means for example, let’s say your house is appraised at $100,000, you’re taxed on $70,000 of that.

Mill Rate

But what is the actual tax rate you’ll pay? Well it depends on where you live. Each local community, based on its budget, has a mill rate (or tax rate) that determines how much you’ll pay. One mill is equal to $1 of tax for every $1,000 of assessed value.

The mill rates range across the region, but in general if you have a higher mill rate, that means each individual property is responsible for a higher share of the budget.

Let’s look at an example to show you what this looks like.

Let’s say a city’s mill rate is 20 mills and your house is appraised at $100,000, meaning your assessed value is $70,000.

The mill rate formula is (assessed property value x mill rate) / $1000 = property tax bill.

($70,000 x 20) / 1,000 = $1,400 for a property tax bill.

How do these parts all work together?

The grand list serves as the foundation for calculating how much tax revenue a town can collect. The communities with wealthier grand lists often have lower mill rates, because they can have higher property values to tax.

For example, the average home price in Greenwich, which has the lowest mill rate, is $2.27 million. Using the 2025-2026 mill rates, Greenwich had a mill rate of about 12.

Using the mill rate formula:

($1,589,000 x 12) / 1,000 = $19,068

Meanwhile, in Bridgeport, which has the highest mill rate in the region, the average home price is $355,127. Using the 2025-2026 mill rates, Bridgeport had a mill rate of 43.45.

Using the mill rate formula:

($248,589 x 43.45) / 1,000 = $10,801

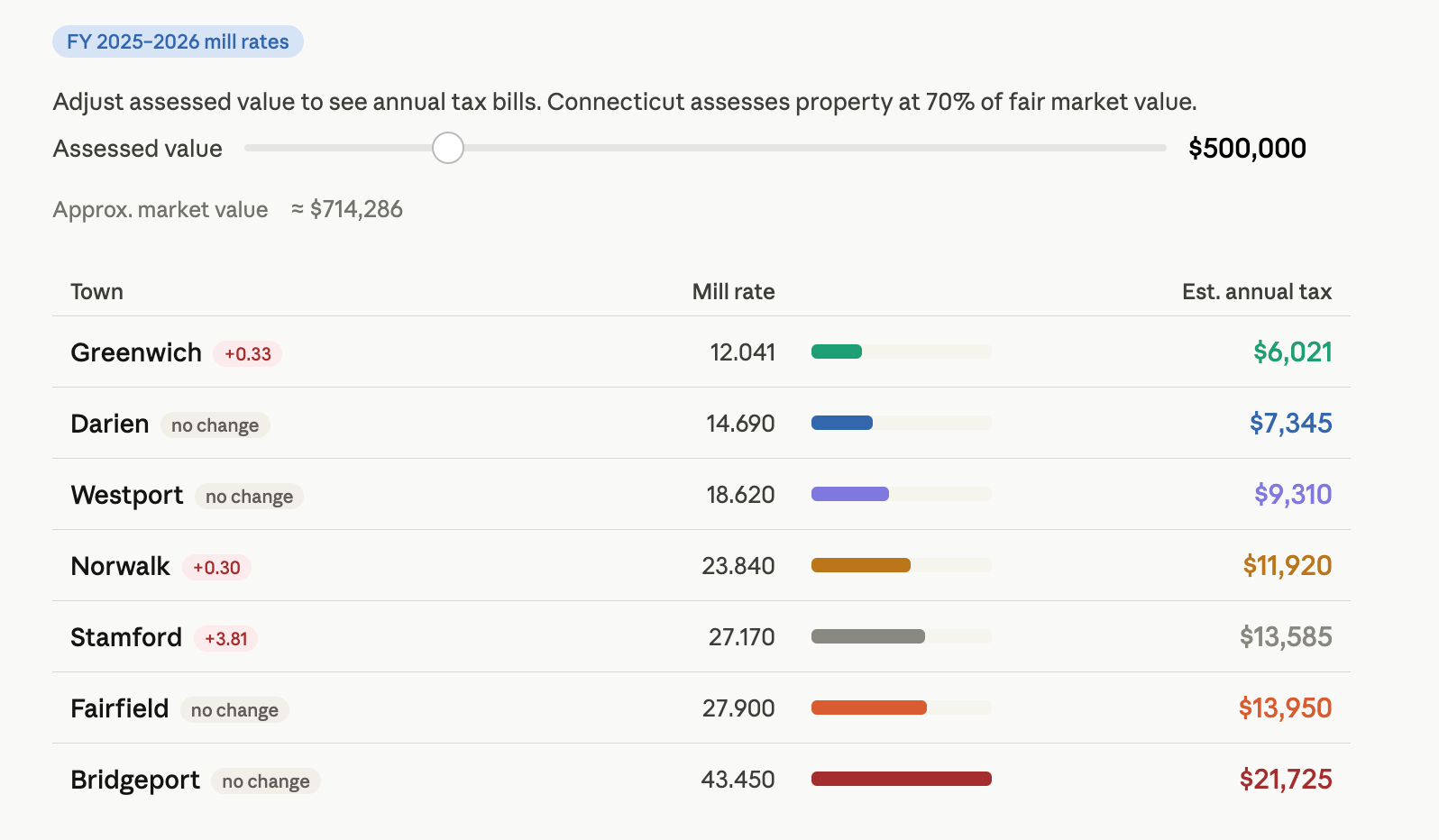

Here’s a look at what the mill rates were last year across the region. You can see how if a property was valued at $500,000 in each town what the estimated annual tax would be.

For communities, like Greenwich, where a $500,000 home is far below the median home price (and extremely hard to find), the owner would pay significantly less in taxes than a homeowner in Bridgeport.

This means that communities with higher grand lists and lower mill rates can make investments without overtaxing residents.

Still, Bridgeport residents in particular could see some improvement in the mill rate this year. Mayor Joe Ganim announced that the city’s grand list had grown 62.5% to $13 billion, which would allow the mill rate to be reduced from 43.45 to 27.75, “the lowest level Bridgeport has seen in decades,” according to the mayor’s office.

“This budget is a gamechanger for Bridgeport,” Ganim wrote in a statement. ”Our city’s growth has outpaced most of Connecticut, signaling a high level of investment and confidence in our future. This budget not only proposes the lowest mill rate in decades but makes the largest investment ever in our schools and libraries, expands senior and veteran tax relief, gives residents free access to our parks, and funds the expansion of supervised balloting. I look forward to working with the City Council on final approval of these proposals.”

Stay tuned for an in-depth look at each community’s budget and what it means for residents.